- EU and UK automotive leaders unite to call for urgent agreement of an ambitious free trade deal before the end of the transition period in just 15 weeks’ time.

- New calculations show the catastrophic impact of ‘no deal’ with WTO tariffs putting production of some 3 million EU and UK built cars and vans at risk over next five years.

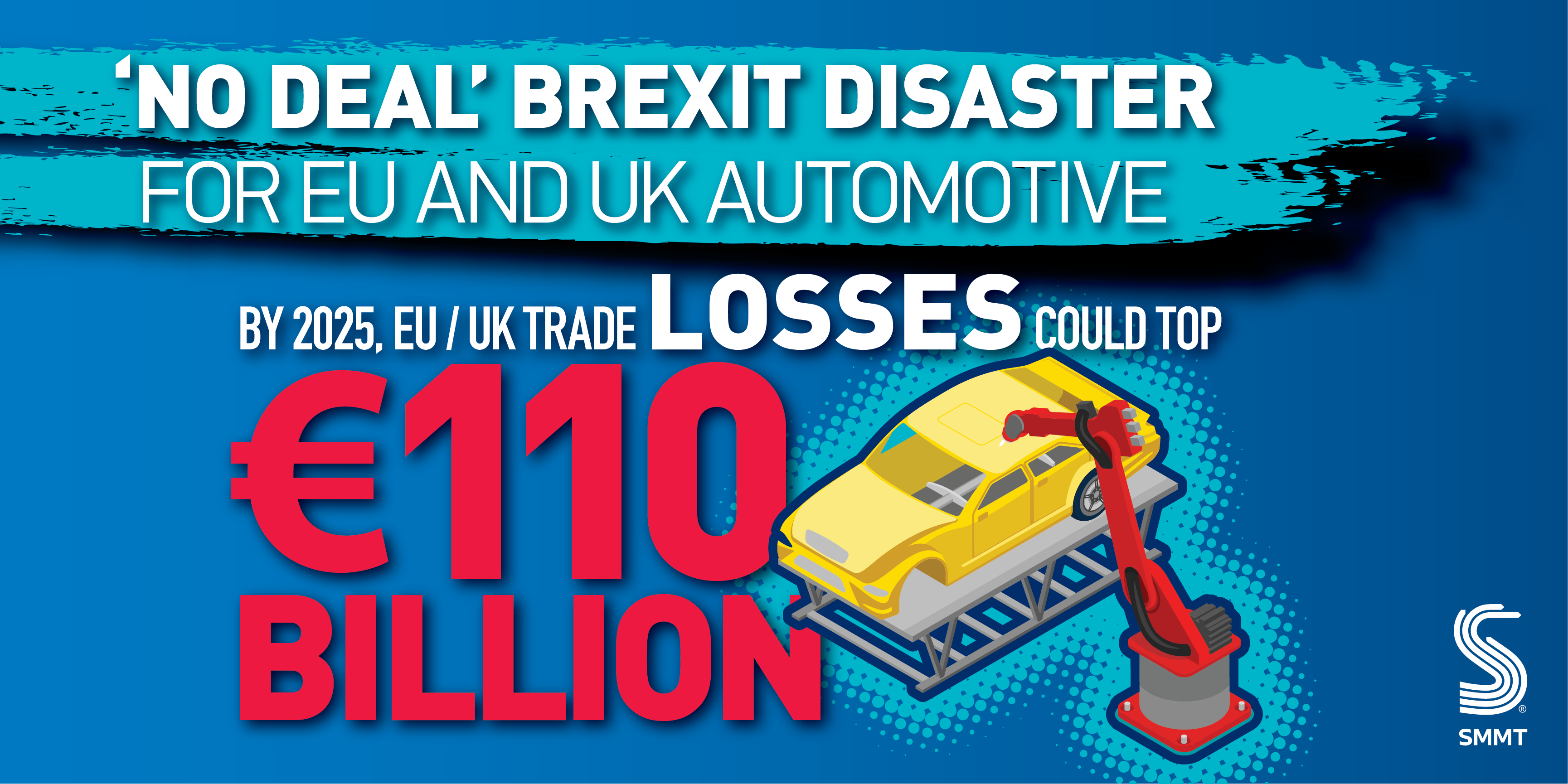

- ‘No deal’ would mean combined EU-UK trade losses worth up to €110 billion to 2025, on top of around €100 billion in lost production value so far this year because of coronavirus crisis.

- To avoid second economic hit to sector employing 14.6 million people, industry calls for negotiators to secure a deal urgently that delivers zero tariffs, modern rules of origin and avoids different regulations across the channel.

With just 15 weeks before the Brexit transition period expires, European automotive industry leaders have today joined forces to call for the EU and UK to secure an ambitious free trade agreement (FTA) without further delay. Negotiators on both sides must now pull out all the stops to avoid ‘no deal’ at the end of the transition, which according to new calculations would cost the pan-European automotive sector some €110 billion in lost trade over the next five years,1 putting jobs at risk in a sector that supports 14.6 million livelihoods, representing one in 15 of EU and UK jobs.2

The lead organisations representing vehicle and parts makers across the EU, the European Automobile Manufacturers Association (ACEA) and the European Association of Automotive Suppliers (CLEPA), along with 22 national associations, including the Society of Motor Manufacturers and Traders (SMMT), German Association of the Automotive Industry (VDA), Comité des Constructeurs Français d’Automobiles (CCFA) and La Plateforme automobile (PFA), are today warning that the sector could face severe repercussions. Indeed, economies and jobs on both sides of the channel are at risk of a second devastating hit in the shape of no deal coming on top of around €100 billion worth of production lost so far this year due to the coronavirus crisis.3

Without a deal in place by 31 December, both sides would be forced to trade under so-called World Trade Organisation (WTO) non-preferential rules, including a 10% tariff on cars and up to 22% on vans and trucks.4 Such tariffs – far higher than the small margins of most manufacturers – would almost certainly need to be passed on to consumers, making vehicles more expensive, reducing choice, and impacting demand. Furthermore, automotive suppliers and their products will be hit by tariffs. This will make production more expensive or will lead to more imports of parts from other competitive countries.

Before the coronavirus crisis hit, EU and UK production of motor vehicles was running at 18.5 million units a year.5 This year some 3.6 million units have already been lost across the sector due to the pandemic.6 New calculations suggest that, for cars and vans alone, a reduction in demand resulting from a 10% WTO tariff could wipe some three million units from EU and UK factory output over the next five years, with losses worth €52.8 billion to UK plants and €57.7 billion to those based across the EU.7 Suppliers would also suffer from these changes.

This combined loss in trade value would seriously harm revenues for a sector that is one of Europe’s most valuable assets, employing millions of people and generating shared prosperity for all, with a combined trade surplus of €74 billion with the rest of the world in 2019. Collectively, the EU27 and UK automotive sector is responsible for 20% of global motor vehicle production and spends some €60.8 billion on innovation per year, making it Europe’s largest R&D investor.8

Achieving an ambitious EU-UK FTA with automotive-specific provisions is critical to the European automotive industry’s future success. Any deal should include zero tariffs and quotas, appropriate rules of origin for both internal combustion engine and alternatively fuelled vehicles, plus components and powertrains, and a framework to avoid regulatory divergence.

Crucially, businesses need detailed information about the agreed trading conditions they will face from 1 January 2021 to make final preparations. This, combined with targeted support and an appropriate a phase-in period that allows for greater use of foreign materials for a limited period of time, will ensure businesses are able to cope with the end of the transition period.

Eric-Mark Huitema, ACEA Director General, said,

The stakes are high for the EU auto industry – we absolutely must have an ambitious EU-UK trade agreement in place by January. Otherwise our sector – already reeling from the COVID crisis – will be hit hard by a double whammy.

Sigrid de Vries, CLEPA Secretary General, said,

A ‘no deal’ Brexit would disrupt the integrated automotive supply chain and hit industry at a critical moment. The impact will be felt far beyond the bilateral trade streams alone, translating into a loss of jobs and investment capacity. The automotive sector is the EU’s largest private R&D investor with €60 billion invested each year. We need a deal that maintains the sector’s global competitiveness.

Mike Hawes, SMMT Chief Executive, said,

These figures paint a bleak picture of the devastation that would follow a ‘no deal’ Brexit. The shock of tariffs and other trade barriers would compound the damage already dealt by a global pandemic and recession, putting businesses and livelihoods at risk. Our industries are deeply integrated so we urge all parties to recognise the needs of this vital provider of jobs and economic prosperity, and pull out every single stop to secure an ambitious free trade deal now, before it is too late.

Hildegard Müller, President of VDA, said,

The automotive industry needs stable and reliable framework conditions. It would be to the great disadvantage of both sides if the UK withdrawal were to end with the application of tariffs in mutual trade. This would jeopardise closely linked value chains and possibly make them unprofitable. Our member companies have more than 100 production sites in the United Kingdom. We hope that the EU and the UK will continue their close partnership – with a comprehensive free trade agreement.

Thierry COGNET, President of CCFA, said,

A ‘no deal’ situation on 1 January 2021 would be particularly challenging for manufacturers. What we need from negotiators, in an economic context already very affected by the COVID crisis, is a substantial deal protecting us from tariffs, quotas and regulatory divergence.

Luc CHATEL, President of PFA, said,

The economic reality is that both manufacturers and suppliers will be very affected by ‘no deal’ and many jobs are at stake. ‘No deal’ would be the worst of all outcomes.

Gianmarco Giorda, ANFIA Director said,

The UK is one of the main trade partners for the Italian automotive industry, the third destination market for parts and components for motor vehicles with the highest positive trade balance (1.34 billion Euros in 2019) and the fourth for cars. As the pandemic has clearly shown, there is a strong supply chain connection among European automotive countries and the relationship between Italian component suppliers and UK local OEMs is inalienable in such a critical moment of slow recovery. As a consequence, the point is avoiding the introduction of new customs tariffs, longstanding procedures and so higher prices, safeguarding both Italian and UK automotive sector competitiveness.

Zdeněk Petzl, Executive Director Czech Automotive Industry Association said,

The insecurities linked to Brexit have already impacted trade relations as the United Kingdom´s position as a destination for Czech automotive exports gradually declined from 2nd to 5th place during the last three years. A no-deal Brexit will have further unprecedented negative effects on the final producers of vehicles as well as parts suppliers, which is something Europe´s economy simply cannot afford given the current economic situation. The imposition of tariffs, diverging legislative requirements and complications in logistics would cause price increases which would eventually be borne by customers on both sides of the Channel.

Brian Cooke, SIMI Director General said,

A no deal outcome would have would be extremely negative for the business relationships between the EU and the UK, adding unnecessary costs and logistical barriers. A solution for reaching an agreement that allows for tariff free and full market access simply must be found.

The 24 Automotive Association signatories include:

- ACAROM – Romanian Association of Automobile Builders www.acarom.ro

- ACEA – European Automobile Manufacturers Association www.acea.be

- ACS – Automotive Cluster of Slovenia www.acs-giz.si/en

- AFIA – Portuguese Manufacturers Association for the Automotive Industry www.afia.pt

- AIA – Czech Automotive Industry Association www.autosap.cz

- ANFIA – Italian Association of the Automobile Industry www.anfia.it

- AUTIG – Danish Automotive Trade & Industry Federation www.autig.dk

- BIL SWEDEN – Swedish Association of Automobile Manufacturers and Importers www.bilsweden.se

- CCFA – Committee of French Automobile Manufacturers www.ccfa.fr

- CLEPA – European Association of Automotive Suppliers www.clepa.eu

- FEBIAC – Belgian and Luxembourg Federation of Automobile and Motorcycle Industries www.febiac.be

- FKG – Scandinavian Automotive Supplier Association www.fkg.se

- FFOE – Austrian Association of the Automotive Industry www.fahrzeugindustrie.at

- ILEA – Luxembourg Automotive Suppliers Association www.ilea.lu/

- MGE – Hungarian Vehicle Importers Association www.mge.hu

- PFA – French Association of the Automotive Industry www.pfa-auto.fr/

- RAI – Dutch Association for Mobility Industry www.raivereniging.nl

- SDCM – Polish Association of Automotive Parts Distributors and Producers www.sdcm.pl

- SERNAUTO – Spanish Association of Automotive Suppliers www.sernauto.es

- SIMI – Society of the Irish Motor Industry www.simi.ie/en

- SMMT – Society of Motor Manufacturers and Traders www.smmt.co.uk

- TAYSAD – Automotive Suppliers Association of Turkey www.taysad.org.tr

- VDA – German Association of the Automotive Industry www.vda.de

- ZAP – Automotive Industry Association of the Slovak Republic www.zapsr.sk

Outline footnotes

1: SMMT calculations covering cars and LCVs. Ave FX rate of Aug 2020 of £- € @1.110715. Based on imposition of 10% tariff = 6.3% price rise = 18.9% drop in demand. Uses average new car and LCV prices based on JATO data.

2: ACEA pocket guide 2020 / 21

3: SMMT & ACEA calculations, IHS Markit LV Production Recovery Tracker (July 2020)

4: UK Global Tariff (10% for cars / vans) & EU Common External Tariff (10-22% dependent on category and tonnage)

5: ACEA pocket guide 2020 / 21 includes cars, vans and HGVs

6: ACEA pocket guide 2020 / 21 (passenger vehicles and LCVs only)

7: SMMT calculations covering cars and LCVs. Ave FX rate of Aug 2020 of £- € @1.110715. Based on imposition of 10% tariff = 6.3% price rise = 18.9% drop in demand. Uses average new car and LCV prices based on JATO data.

8: ACEA pocket guide 2020 / 21