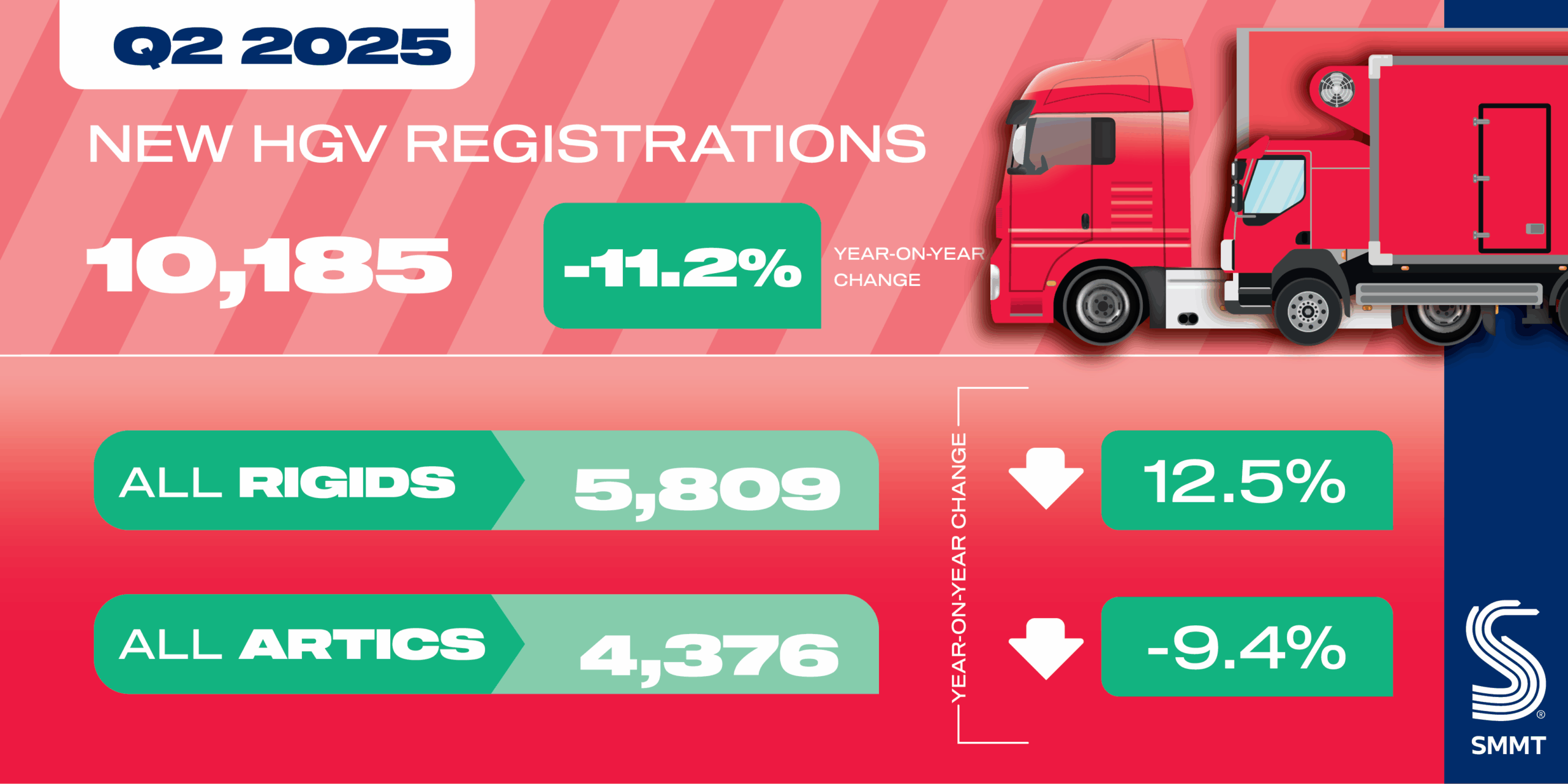

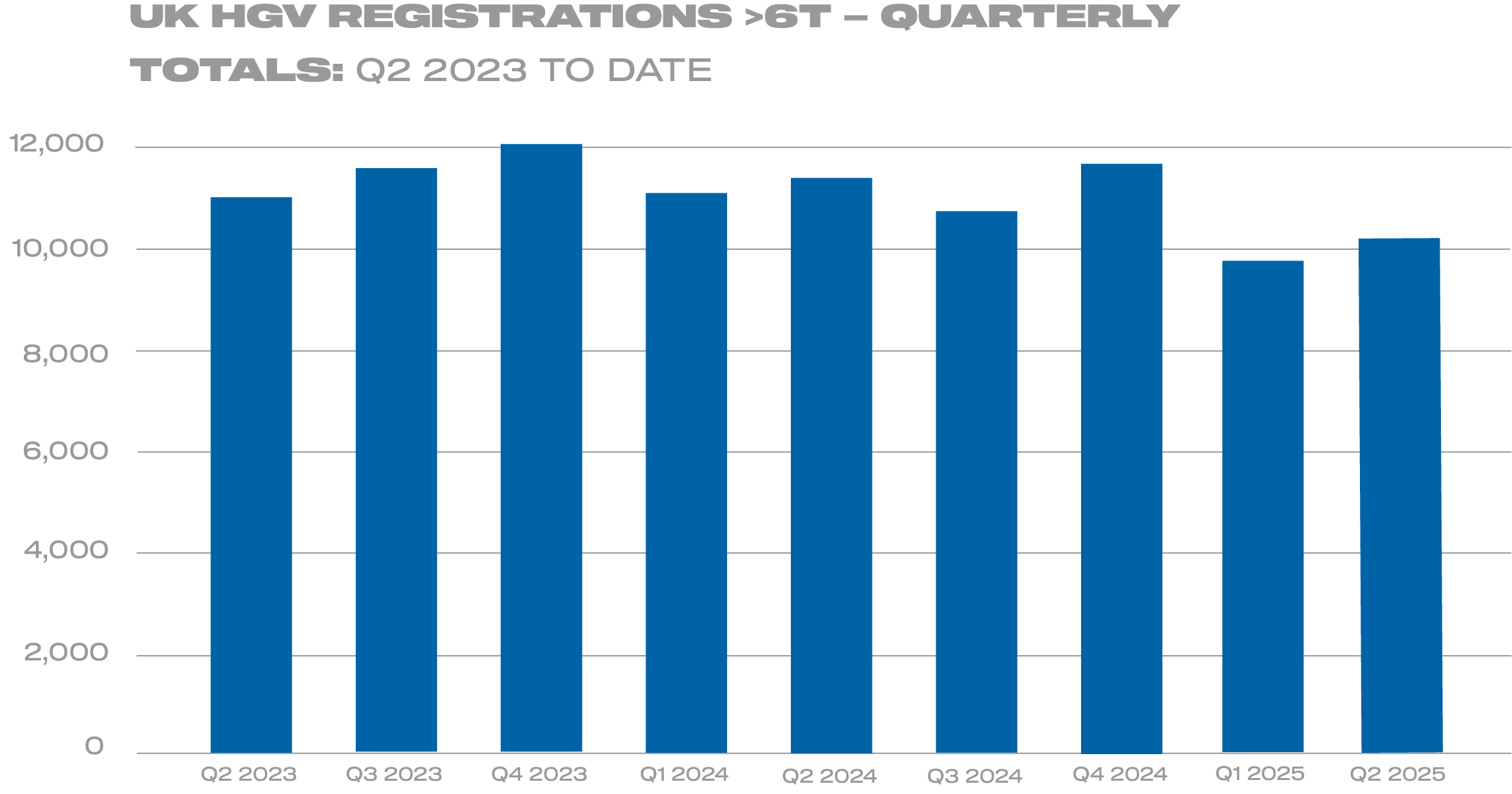

- New heavy goods vehicle uptake declines -11.2% in Q2 as fleet renewal continues to normalise.

- Demand falls across all body types bar refuse trucks, but tractors remain most popular.

- ZEV rollout up 59.1% during first half with record 0.9% share – but equivalent to fewer than 200 units.

- Industry welcomes new depot infrastructure grants, with grid reform now needed to unblock rollout.

Data download

Heavy goods vehicle (HGV) registrations fell by -11.2% in the second quarter of 2025, with 10,185 new trucks joining UK roads, according to the latest figures published today by the Society of Motor Manufacturers and Traders (SMMT). The decline, amid a tough economic environment, reflects the cyclical nature of fleet renewal as the new HGV market continues to normalise following a three-year period of robust growth after the pandemic.1

The Q2 decline was driven by an -8.1% drop in demand for new tractor units – still representing more than two fifths (42.2%) of the market – with 4,295 registered, as well as a -33.1% fall in box vans, to 905 units. Deliveries of new tippers and curtain-siders also declined, by -19.6% and -24.2% to 795 and 781 units respectively. Registrations of refuse collection vehicles, meanwhile, bucked the trend, rising 11.4% to 614.

Demand for new zero emission HGVs also grew, up by 32.3% in the quarter, with registrations in the first half of 2025 rising 59.1% compared with the same period last year. Volumes remain small, however, with 183 units registered across the first six months – a market share of 0.9%. Fleet decarbonisation is moving in the right direction but with the UK aiming to have all new HGVs weighing up to 26 tonnes zero emission by 2035, the rate of uptake will need to grow rapidly.

Manufacturers are delivering huge choice for fleet operators, with 35 different zero emission models already on the market and able to meet a wide range of use cases. However, the upfront cost of switching remains a barrier – particularly the investment capital required to install depot infrastructure for chargepoints.

The industry welcomes government’s grant support for depot upgrades announced in July which will be a key enabler for more fleets to make the transition. Getting that funding into the ground now requires another challenge to be overcome, with current planning processes resulting in grid connection waits of up to 15 years – beyond the 2040 end of sale date for all non-zero emission vehicles.

Given decarbonising road transport is fundamental to the UK’s wider net zero ambitions, transport depots must be afforded the same fast-tracking priority to grid connections as that recently announced for data centres, wind farms and solar.2 A longer term national strategy that delivers public, HGV-suitable infrastructure across every region is also needed so that all fleets can plan investment into zero-emission fleet development.

Another quarter of decline in the new HGV market is unsurprising as the market continues to normalise, but a return to growth must happen soon, given this sector is a crucial driver of the UK economy. The highest market share yet for zero-emission trucks is positive, albeit it still represents less than one percent of the market with many operators just one buying cycle from end of sale deadlines.

New depot infrastructure funding is welcome, and grid reform must now follow so that operators can get the chargepoints they need to confidently invest in their fleets.

Notes to editors

1 HGV registrations growth 2021: 12.9%; 2022: 9.6%; 2023: 13.5%

2 DESNZ, 15 April 2025