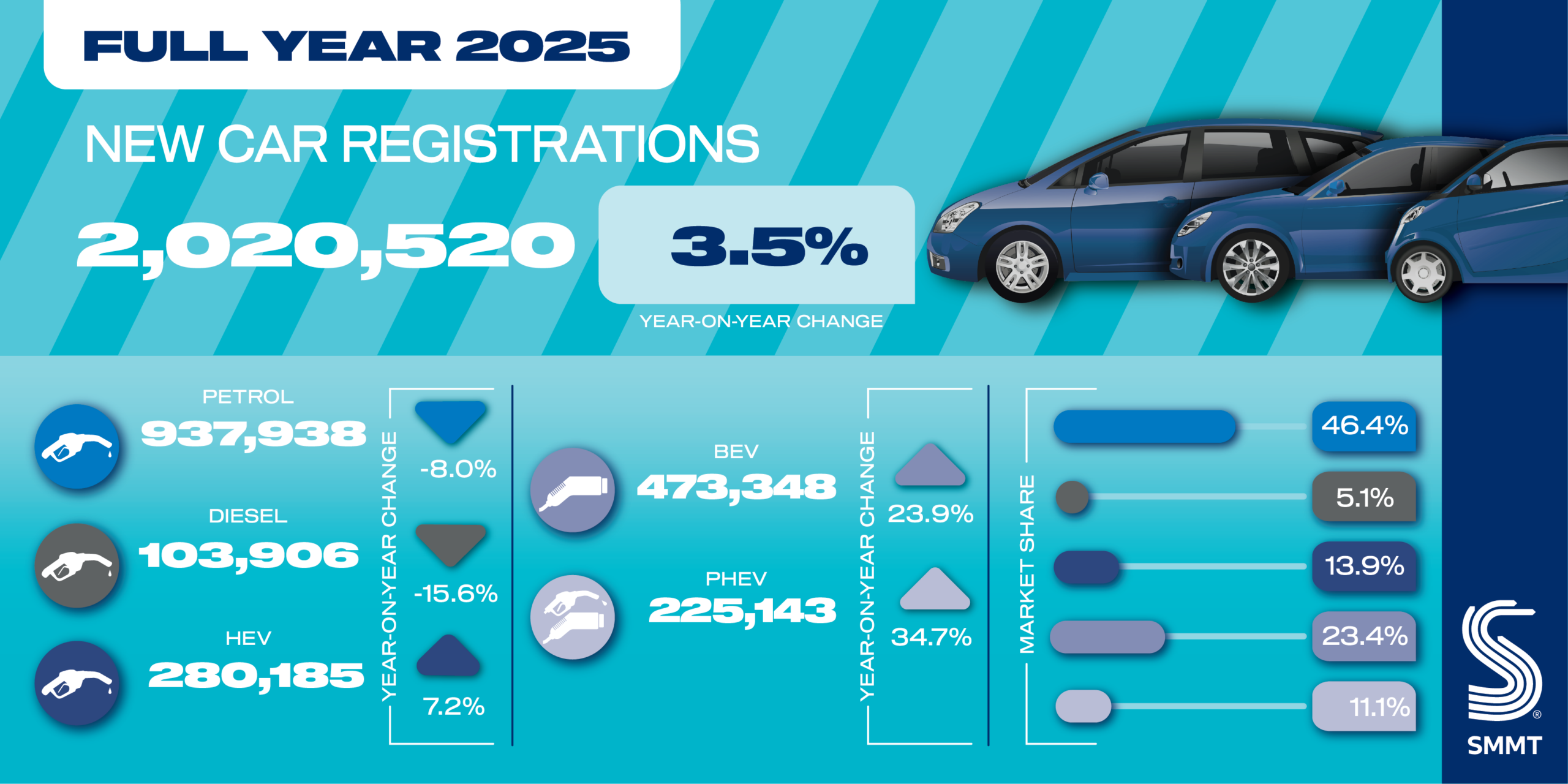

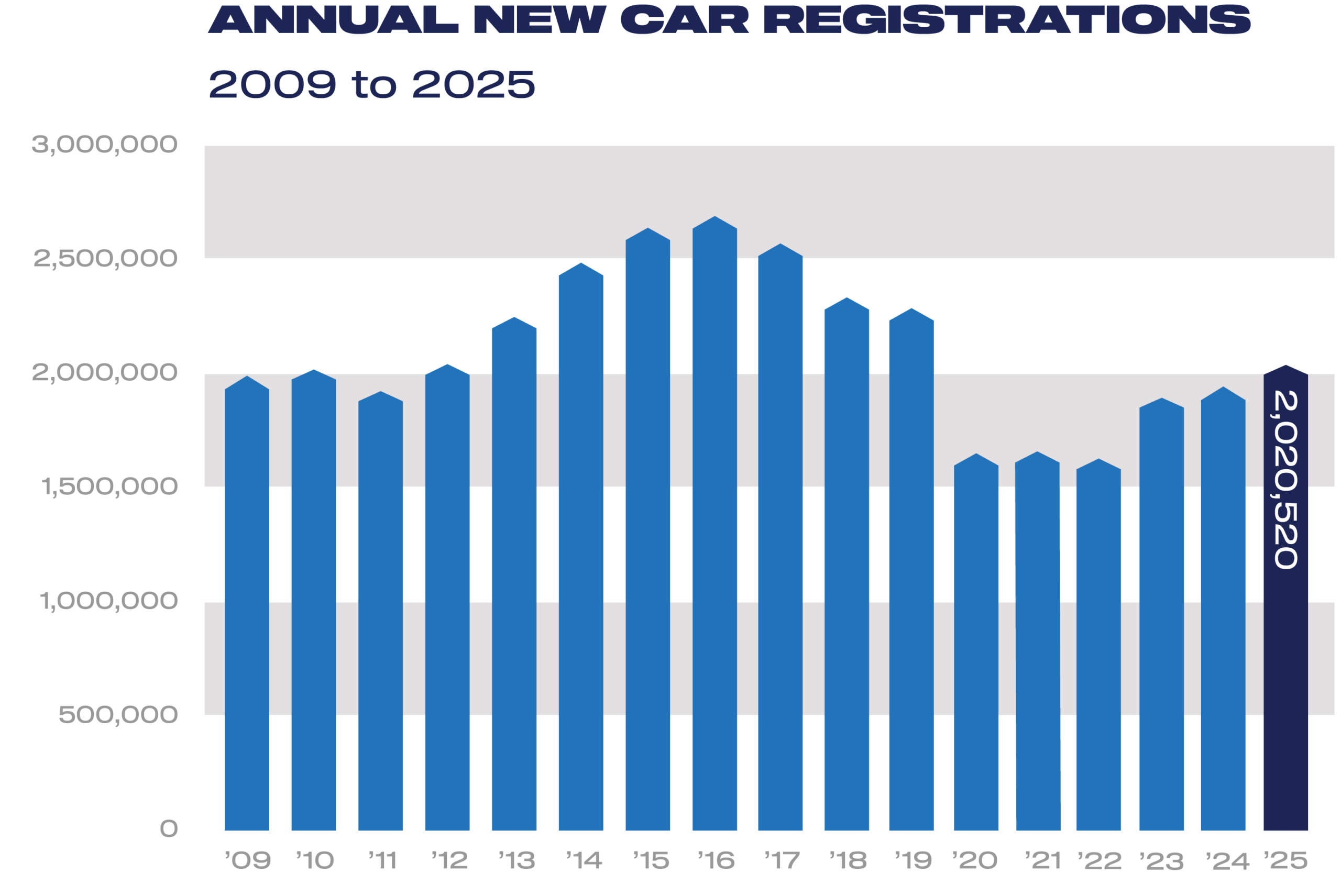

- New car registrations reach 2.02 million in 2025 with market up 3.5% year on year.

- Internal combustion engine still biggest selling powertrain but growing demand for electrified cars narrows majority to just 51.5%.1

- Almost half a million new BEVs join the road as around one in four buyers go electric – but gap between demand and ambition widens.

- Industry urges government to bring forward review to support industry competitiveness and sustainability.

Data download

New car registrations data December 2025

The UK new car market grew for the third year in a row in 2025, breaching the two million mark for the first time since the pandemic, with 2,020,520 new car registrations, according to the latest figures from the Society of Motor Manufacturers and Traders (SMMT).

Uptake in December rose by 3.9% to 146,249 units, with a final flourish in the private buyer market, up by 16.0%. Repeating a pattern seen in previous years,2 battery electric vehicle (BEV) registrations took a high market share in the final month of the year, accounting for 32.2% of the market – the only time the ZEV mandate target of 28% was exceeded in 2025.

As a result, last year’s market rose by 3.5%, with growth across all buyer types. Demand from private buyers recovered slightly from 2024 – when uptake fell below levels last seen during 2020 – with a 4.5% increase to 779,587 units, but still only comprising 38.6% of registrations. Fleet and business registrations also rose, up 2.6% to 1,194,545 and 8.8% to 46,388 respectively.

Electrified vehicles narrowly missed becoming the majority of the market despite a surge during the last quarter. Hybrid electric vehicle (HEV) volumes rose by 7.2% to achieve a 13.9% market share, while plug-in hybrids were the fastest growing powertrain, with volumes increasing 34.7% to take 11.1% of registrations.

Meanwhile, almost half a million (473,348) new BEVs were registered during 2025 – more than in the whole of 2021 and 2022 combined. This huge volume, which is likely to place the UK as the second biggest EV market in Europe by volume, saw BEV market share rise to reach 23.4% – a strong uplift, but with a mandate target of 28% the gap between demand and ambition is increasing rather than diminishing.3

Massive manufacturer investment now provides a choice of more than 160 BEV models – up from just over 130 at the start of 2025 – with at least 60 more due in 2026. However, EV uptake has risen by only 23.9%. The long-awaited return of a grant for EV purchase has helped, although only around a quarter of models are currently eligible for the incentive at any level. It is manufacturers, therefore, that continue to shoulder the burden of driving up demand, subsidising their sale by more than £5 billion in 2025, equivalent to a massive £11,000 per BEV registered.4 Such subsidies are clearly unsustainable. Furthermore, the announcement of a new ‘eVED’ tax on EVs purchased from 2028 sends a confusing message to consumers, undermining rather than encouraging market confidence.

While average new car CO2 has fallen by -10.1% from 2024 to 91.8 g/km, which will assist some manufacturers with mandate compliance, the UK’s zero emission sales target will next year require BEVs comprise one in three new car registrations. The UK already has the most ambitious transition trajectory of any major market and, with the EU’s proposal to revise its end of sale date from 2035, divergence between the UK and the much larger market on its own doorstep is broadening.

Action is needed from government to ensure the British market remains attractive for investment, and one which supports consumers, the industry and the economy. The forthcoming review of the ZEV Mandate will be a crucial opportunity to ensure the transition supports the UK’s international competitiveness and prosperity, as well as its shared decarbonisation goals.

Mike Hawes, SMMT Chief Executive

The new car market finally reaching two million registrations for the first time this decade is a reasonably solid result amid tough economic and geopolitical headwinds. Rising EV uptake is an undoubted positive, but the pace is still too slow and the cost to industry too high. Government has stepped in with the Electric Car Grant, but a new EV tax, additional charges for EV drivers in London and costly public charging send mixed signals. Given developments abroad, government should bring forward its review and act urgently to deliver a vibrant market, a sustainable industry and an investment proposition that keeps the UK at the forefront of global competition.

Notes to editors

- ‘Electrified’ is defined as hybrid electric vehicles (HEVs), plug-in hybrid vehicles (PHEVs) and battery electric vehicles (BEVs) combined. Combined petrol and diesel share 2024: 58.5%

- BEV registrations: Dec 2022: 32.9%; Dec 2024: 31.0%

- 2024 BEV share 19.6% vs mandate target of 22% – difference of 2.4pp. 2025 BEV share 23.4% vs mandate target of 28% – difference of 4.6pp

- Based on SMMT analysis of AutoTrader data on EV discounts, SMMT estimated fleet discounts and EV car market data, and JATO sales weighted recommended retail price data

SMMT Update

Sign up

Sign up to the SMMT Update Newsletter for weekly automotive news and data

"*" indicates required fields