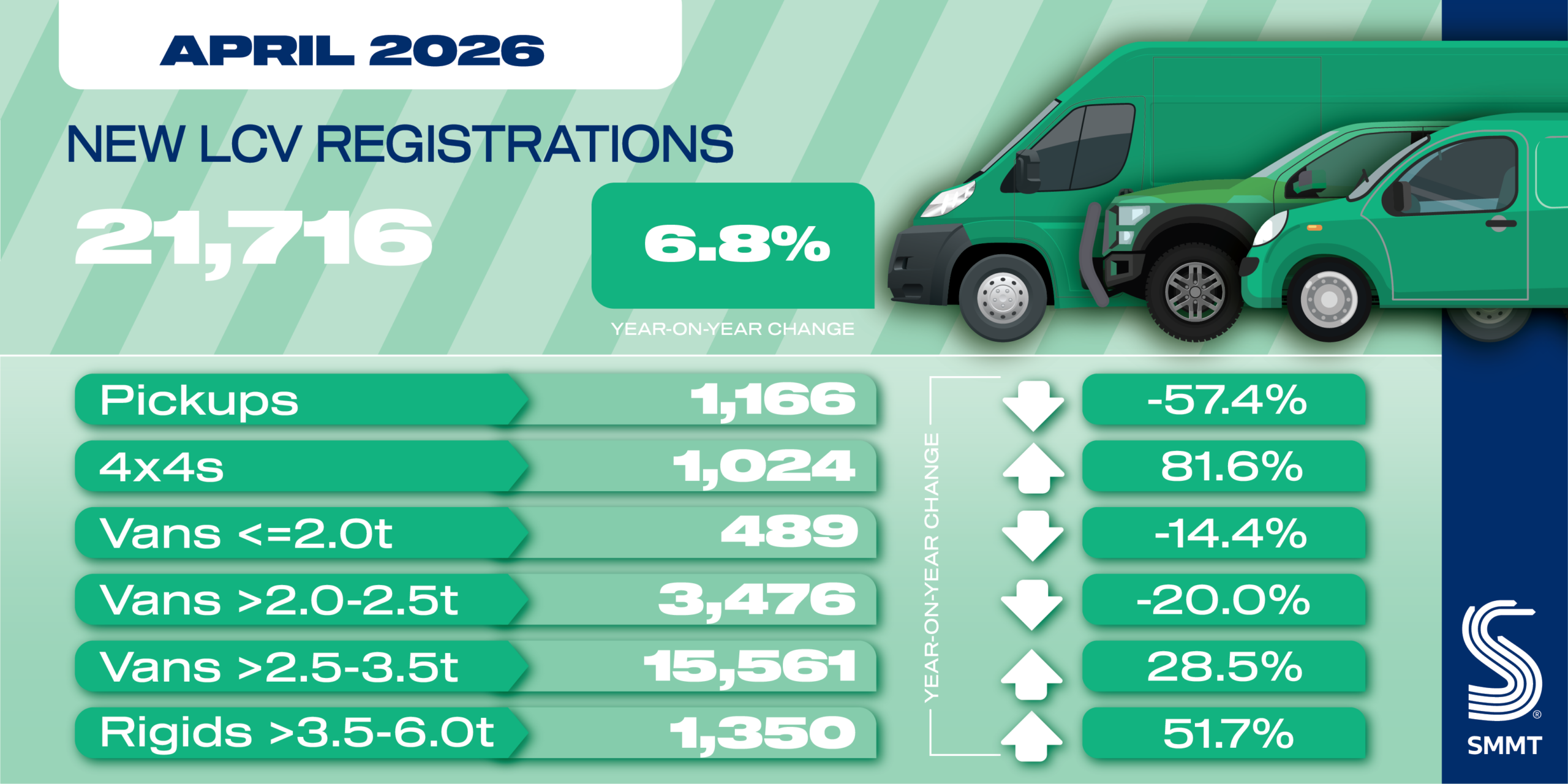

- 21,716 new vans, pickups and 4x4s join UK roads in April, up 6.8% year on year.

- Growth driven by 28.5% rise in large vans but pickups continue to slump, down -57.4%.

- Zero emission uptake rises 44.7% but market share still under half of 24% mandated.

- Latest industry outlook expects full-year market to be flat (-0.5%) with BEVs at 11.1% share.

Data download

new LCV registrations April 2026

The new light commercial vehicle (LCV) market rose by 6.8% in April with 21,716 vans, pickups and 4x4s joining UK roads, according to the latest figures published today by the Society of Motor Manufacturers and Traders (SMMT). While the performance is compared against a weak April last year – a month impacted by tax changes – the return to growth after a disappointing March is welcome.1

Performance was mixed, with overall growth driven by deliveries of large vans, up 28.5% to 15,561 units, representing 71.7% of all new LCVs registered. Medium-sized vans declined, meanwhile, by

-20.0% to 3,476 units. In the smaller volume segments, registrations of 4x4s rose by 81.6% to 1,024 units, while small vans fell -14.4% to 489 units.

Demand for pickups slumped again, down -57.4% to just 1,166 units, rounding off volume declines in 11 of the past 12 months – the result of last April’s fiscal changes to treat double cabs as cars for Benefit in Kind purposes.2 While double cab VED and VAT rules remain the same, the BIK measure is heaping additional costs on crucial business sectors such as farming and construction. Industry continues to urge government to reverse the measure and unlock investment in the latest, increasingly zero emission models – getting older and more polluting vehicles off the road while boosting Treasury tax receipts.

More positively, demand for battery electric vans (BEVs)3 grew strongly following a decline in March, up 44.7% with 2,439 registrations in April. At an 11.1% market share, however, BEV adoption represented less than half the 24% share mandated for 2026. More than half of the UK’s LCV model offering is currently available with a plug, backed by substantial manufacturer discounts and government’s Plug-in Van Grant – yet the higher upfront cost of BEV fleet renewal, rising energy costs and infrastructure challenges remain barriers to greater uptake.

With the year-to-date BEV share still just 9.4%, the sector continues to call for an urgent and holistic review of the transition – ensuring the regulation reflects market realities and operators have the additional support they need to accelerate zero emission adoption.

Mike Hawes, SMMT Chief Executive

April’s improved market is welcome news, despite a tough economic environment. New LCV investment drives growth and decarbonisation, but must be sustained by investment in public and depot BEV infrastructure – and a reversal of BIK on double cabs – to build momentum for fleet renewal that cuts emissions and boosts business.

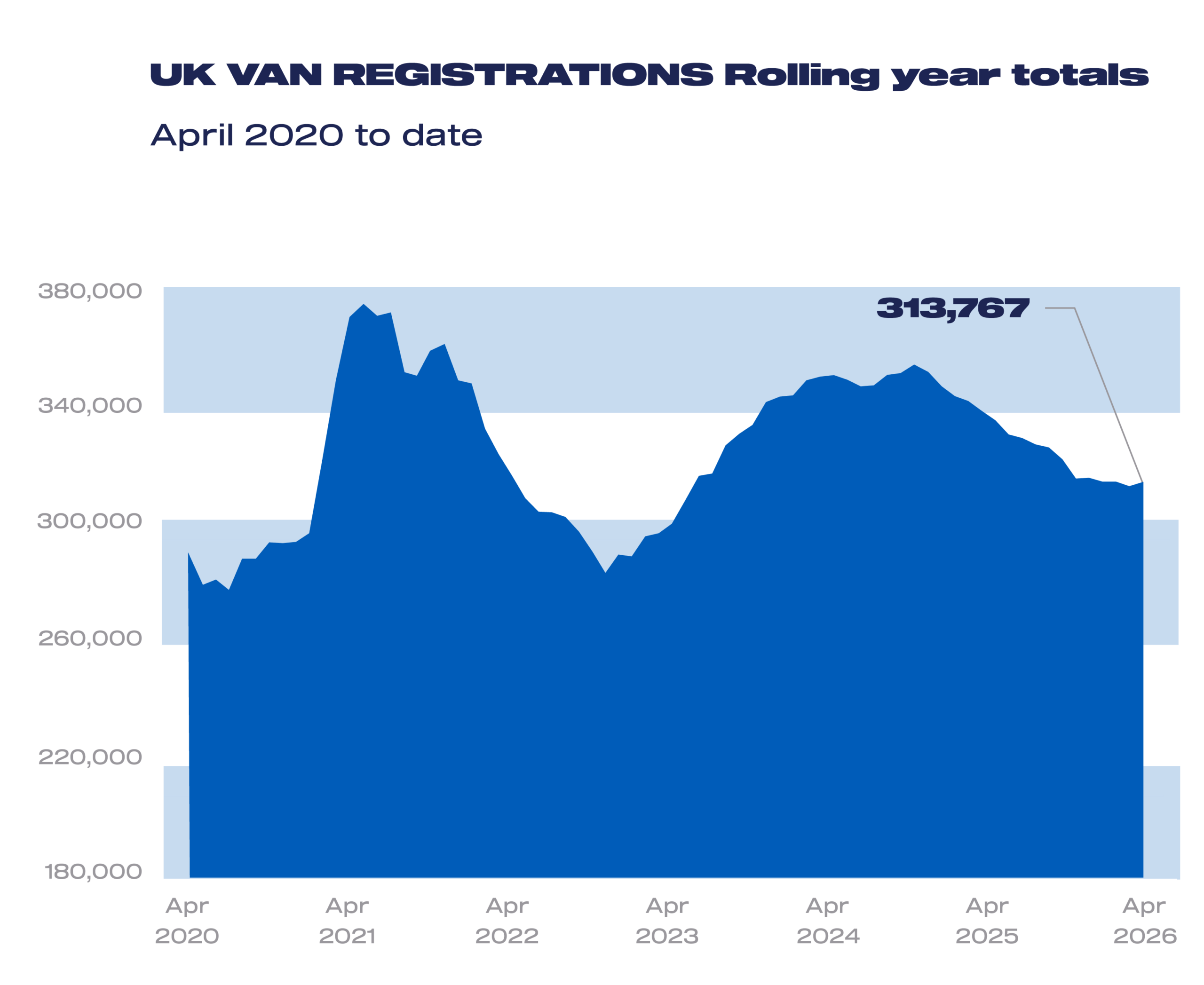

The latest industry outlook for 2026 has been revised downwards, with 314,000 units expected to be delivered this year – flat (-0.5%) compared with last year, and 7,000 units fewer than January’s outlook. BEVs up to 3.5T are expected to see volume growth of 25%, half the level anticipated in January, reaching a market share of 11.1% – considerably adrift of the ZEV Mandate ambition.

Notes to editors

- New LCV registrations, April 2025: -14.9%, 20,332 units; March 2026: -3.4%, 49,505 units.

- September 2025 was the only month of pickup growth, up 7.8% to 5,749 units, due to deliveries of orders placed prior to the BIK change.

- SMMT’s BEV LCV registration data reflects the Vehicle Emissions Trading Scheme, in which BEVs weighing >3.5-4.25t contribute towards each manufacturer’s target, in addition to those weighing ≤3.5t.

SMMT Update

Sign up

Sign up to the SMMT Update Newsletter for weekly automotive news and data

"*" indicates required fields