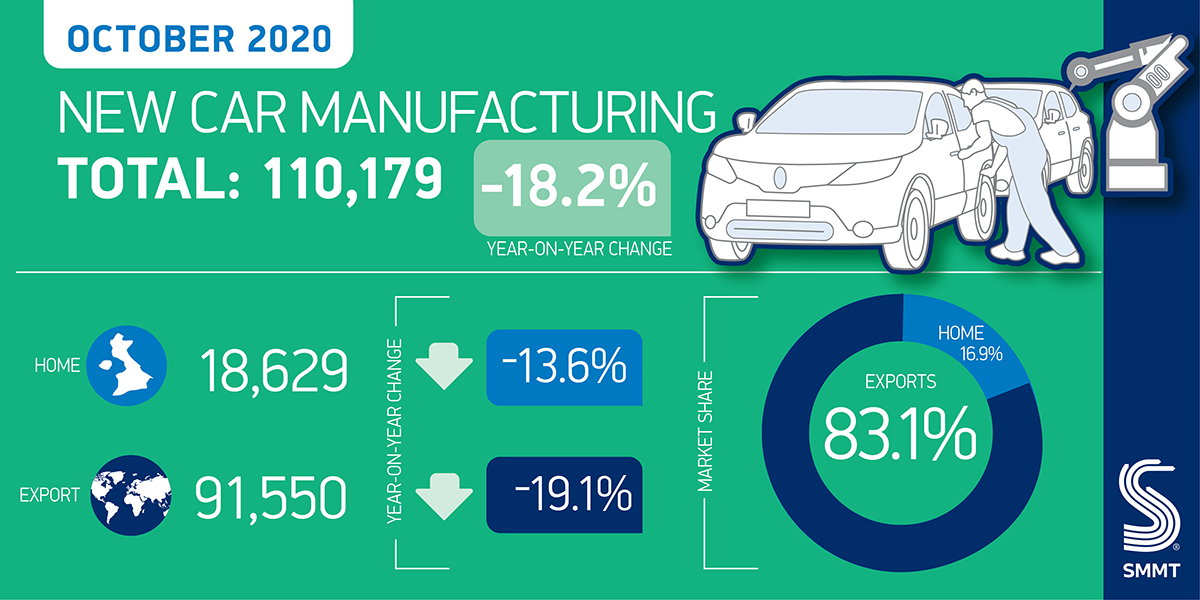

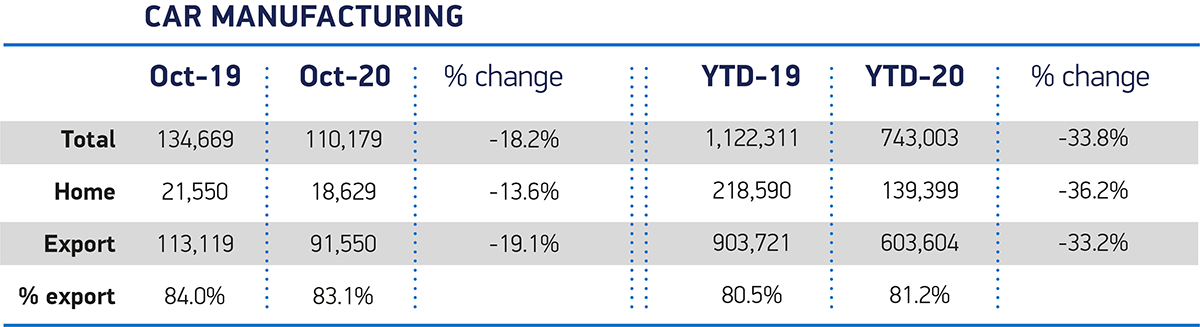

- UK car production falls -18.2% in October with 110,179 units leaving factory gates.

- Subdued demand from EU and US markets drives -19.1% exports decline, as output for UK buyers also falls.

- Year-to-date output lags by -33.8% with 379,308 fewer cars made than same period in 2019.

- Automotive sector calls for urgent Brexit agreement with details shared swiftly, and adequate time to implement the deal, to help companies prepare.

UK car manufacturing output fell -18.2% in October, with 110,179 units leaving factory gates, according to the latest figures issued today by the Society of Motor Manufacturers and Traders (SMMT). This represented 24,490 fewer cars made than in the same month in 2019 with the impact of coronavirus and fresh lockdowns at home and overseas subduing demand in many key markets.

October’s decline was driven largely by falling exports, particularly to the EU and US, down -19.1% overall and equivalent to a loss of 21,569 vehicles. Shipments to the US fell by -26.0% and to the EU by -25.7%. Major Asian markets fared better, with exports to Japan and China up 57.1% and 9.7% respectively, reflecting less stringent lockdown measures, but this was not enough to offset losses elsewhere. Production for the domestic market also fell, by -13.6% to 18,629 units, with 2,921 fewer cars made for buyers in the UK than a year earlier.

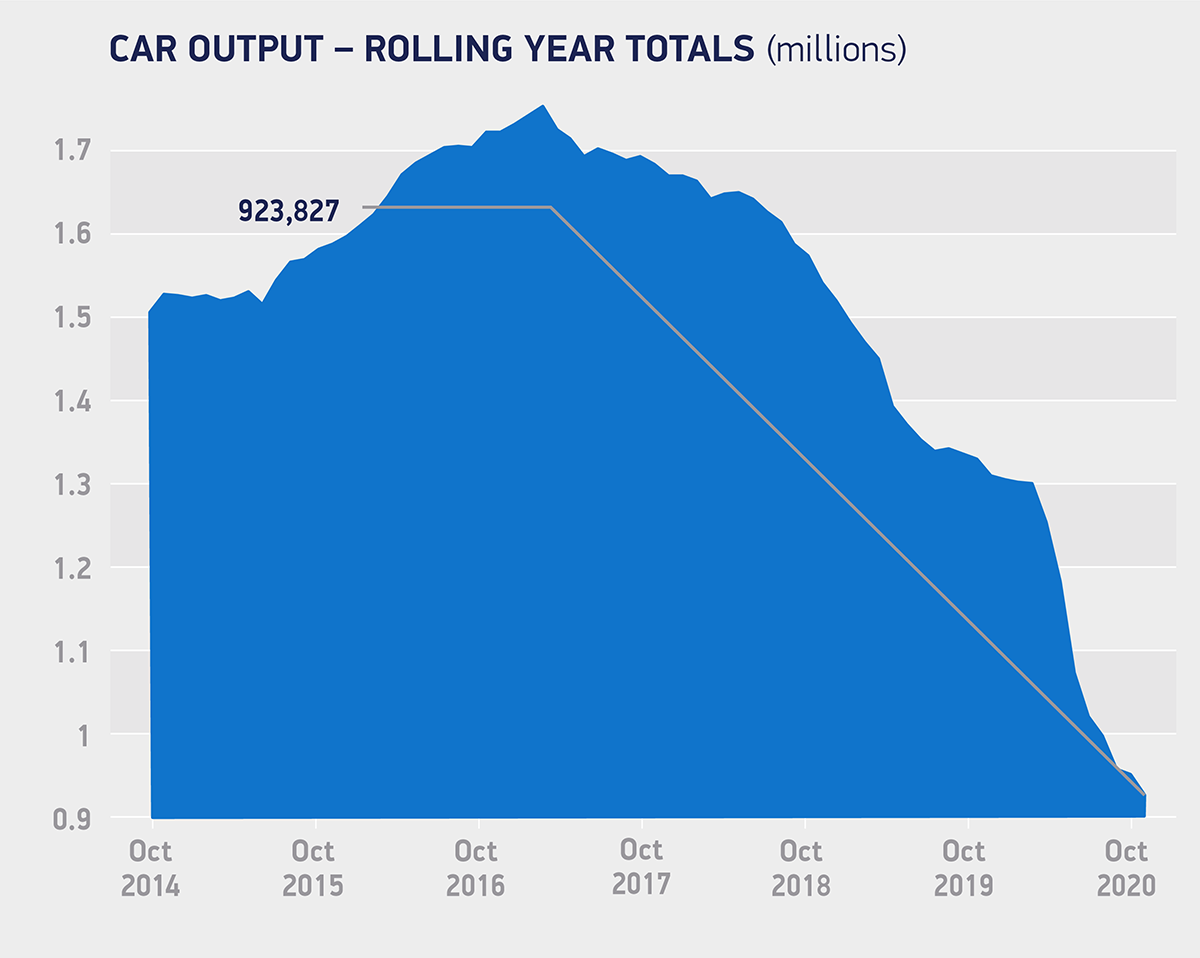

October’s performance rounds off an extremely tough 10 months for UK car makers and suppliers, and production is now down -33.8% since January to 743,003 units – a year on year shortfall of 379,308 units worth some £10.4 billion.1

Mike Hawes, SMMT Chief Executive, said,

These figures are yet more bad news for an industry battered by Covid, Brexit and, now, the unprecedented challenge of a complete shift to electrified vehicles in under a decade. While the sector has demonstrated its resilience, we need the right conditions to remain competitive both as a manufacturing nation and a progressive market. Yesterday’s Spending Review recognised the need to invest in a green industrial revolution, but this must be at globally competitive levels and equal to the scale of ambition to keep this sector match fit. Above all, we must have a Brexit deal, one with zero tariffs, zero quotas and rules of origin that benefit existing products and the next generation of zero emission cars, as well as a phase in period that allows this transition to be ‘made in Britain’.

The news comes as the sector eagerly awaits agreement of a UK-EU trade deal and with new figures revealing the incredible cost of trading with WTO tariffs long-term. In the event of ‘no deal’, production losses could cost as much as £55.4 billion over the next five years, and even with a so-called ‘bare-bones’ trade deal agreed, the cost to industry would be some £14.1 billion.2 For the automotive sector, Brexit has always been about damage limitation and, with a mere 35 days left until the end of transition, the sooner new trading terms are agreed and finer details communicated the better.

Notes to editors

1: SMMT calculations.

2: Independent AutoAnalysis Production Outlook Report November 2020. AutoAnalysis now expects car and van output to fall by more than two million units between 2021-2025 in a WTO scenario with tariffs, compared to a deal with zero tariffs and quotas, which means a loss in value (factory gate prices) of £55.4bn over the five years and £14.1bn with a bare bones deal.